Why Settlement Dates Tripped Me Up Early On

When I first started trading, I thought selling a stock meant the money was immediately mine to use again. I’d close a position, see the cash show up in my account, and go right back to trading it. Then I got hit with a good-faith violation and had to figure out what I’d done wrong.

The answer was settlement. I didn’t understand that a trade executing and a trade settling are two different things, and that difference has real consequences for how you manage your account.

If you’re new to trading, or if you’ve ever wondered why your funds aren’t always available right away, this is the concept you need to understand.

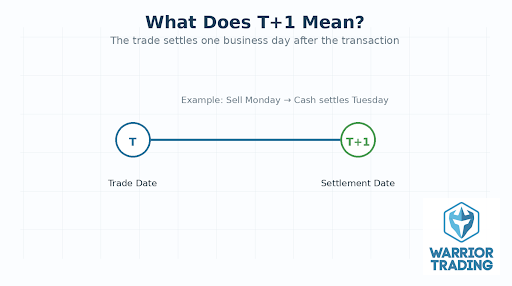

What Does T+1 Day Actually Mean?

The “T” in T+1 stands for transaction date, which is the day you actually execute the trade. The number after the plus sign tells you how many business days after that transaction the trade officially settles.

Settlement is when the buyer officially receives the shares, and the seller officially receives the cash. Until settlement happens, the trade isn’t fully complete from a legal and financial standpoint.

So T+1 means the trade settles one business day after you execute it. T+2 means two business days. T+3 means three business days. Weekends and market holidays don’t count. If you buy a stock on a Friday under T+1, your trade settles on Monday.

It’s a straightforward concept once you see it, but the implications for how you use your capital are significant.

How Settlement Affects Cash Accounts

This is where settlement gets practically important for traders, especially those using cash accounts .

In a cash account, you can only trade with settled funds. When you sell a stock, the proceeds don’t officially settle until T+1. That means if you sell on Monday, you generally can’t use those proceeds to buy another stock until Tuesday.

If you try to buy with unsettled funds and then sell that new position before the original funds settle, you’ve committed what’s called a good faith violation . Get three of those in a rolling 12-month period, and your broker will restrict your account to trading with settled funds only for 90 days.

The move to T+1 actually helped cash account traders in one important way: you only have to wait one business day instead of two before your proceeds are available again. That’s a meaningful improvement if you’re actively trading in a cash account.

Good Faith Violations and Free Riding

Two violations are worth knowing by name.

A good faith violation happens when you buy a security using unsettled funds and then sell it before those funds settle. The key word is “sell.” If you buy with unsettled funds and hold the position past settlement, you’re fine. It’s the act of selling before settlement that triggers the violation.

Free riding is more serious. It happens when you buy a security, sell it for a profit before paying for it, and use the sale proceeds to cover the original purchase. This is prohibited under Regulation T , which governs how brokers extend credit to customers. A free riding violation results in a 90-day cash restriction on your account.

Both of these violations are more common than people realize, especially among newer traders who don’t understand the difference between when a trade executes and when it settles.

How Settlement Works in Margin Accounts

If you’re trading in a margin account , settlement works differently. Your broker extends you credit, which means you can generally buy and sell without waiting for your previous trades to settle. The margin account essentially bridges the gap.

This is one of the reasons many active traders use margin accounts. It gives you more flexibility with your buying power and eliminates most of the settlement timing issues that affect cash accounts.

That said, margin accounts come with their own rules. They require a minimum of $2,000 to open and maintain the account.

If your account has $25,000 or more, you’re subject to the pattern day trader rule , which limits you to three day trades in a rolling five-business-day period unless you maintain that minimum balance . If you’re under $25,000 , understanding settlement in a cash account becomes even more important, because that may be the account type you’re working with.

What T+1 Means for Your Day Trading

For pure day traders who open and close positions within the same session, settlement is mostly a background process. You’re in and out before settlement even becomes relevant.

It matters most in how you manage your capital between trading days. If you close all your positions by EOD, those proceeds settle the next business day under T+1. That’s fast enough that most active traders won’t feel the friction.

Settlement isn’t the most exciting topic in trading, but it’s one of those foundational things that can quietly cause problems if you don’t have it down. Now you do.

FAQs

What is the T 3 payout?

It refers to the obligation in the brokerage business to settle securities trades by the third day following the trade date. The settlement occurs when the seller receives the sales price (the broker’s commission), and the buyer receives the shares.

Can I sell a stock on T1 day?

“T+1” literally stands for Trade date plus one working day. That means if you buy a stock today (T day), you’ll receive those shares in your demat account by the next business day (T+1). Similarly, if you sell shares today, you’ll receive the money in your bank account the next day.